Deed in Lieu of Foreclosure Document for California State

Deed in Lieu of Foreclosure Document for California State

In the complex landscape of real estate transactions, the California Deed in Lieu of Foreclosure form stands out as a vital tool for homeowners facing financial distress. This form provides a way for property owners to voluntarily transfer ownership of their home back to the lender, effectively sidestepping the lengthy and often painful foreclosure process. By opting for this route, homeowners can alleviate some of the stress associated with mounting debt and the threat of foreclosure. The process typically requires the homeowner to meet certain criteria, such as demonstrating financial hardship and being unable to keep up with mortgage payments. Additionally, the lender must agree to accept the deed in lieu as a resolution to the outstanding mortgage debt. This arrangement can benefit both parties: homeowners can avoid the negative impact of foreclosure on their credit scores, while lenders can minimize their losses and expedite the property’s return to the market. Understanding the nuances of this form is crucial for anyone considering it as a viable option, as it involves careful consideration of both the benefits and potential drawbacks.

When considering a Deed in Lieu of Foreclosure in California, it's essential to understand the process and implications. Here are some key takeaways:

By keeping these points in mind, you can navigate the Deed in Lieu of Foreclosure process with greater confidence and clarity.

Will I Owe Money After a Deed in Lieu of Foreclosure - Lenders may consider this option as a way to minimize their losses from defaulted loans.

Understanding the importance of the Missouri Notice to Quit form is essential for both landlords and tenants, as it outlines the necessary steps to be taken when a lease is violated. For further assistance in navigating the intricacies of this form, you can visit https://missouriform.com to obtain a comprehensive guide and resources.

The Loan Servicer Might Agree to Put the Foreclosure on Hold to Give You Some Time to Sell Your Home - This document is an option to consider before falling too deeply into mortgage default.

Deed in Lieu of Mortgage - Homeowners using this form may have to meet specific conditions set forth by the lender.

Deed in Lieu of Forclosure - Be aware that this option might not be available for all mortgage types.

A Deed in Lieu of Foreclosure is a useful tool for homeowners facing financial difficulties. When utilizing this form, several other documents may be necessary to ensure a smooth process. Below is a list of related forms and documents that are often used in conjunction with the California Deed in Lieu of Foreclosure.

Understanding these related documents can help homeowners navigate the complexities of a Deed in Lieu of Foreclosure. Each form plays a vital role in ensuring that both the borrower and lender are protected throughout the process.

When filling out the California Deed in Lieu of Foreclosure form, it's important to be mindful of certain practices that can help ensure a smoother process. Here’s a list of things you should and shouldn’t do:

Filling out a California Deed in Lieu of Foreclosure form can be a complex process, and many individuals make mistakes that can complicate their situation. One common error is failing to provide accurate property information. It is essential to ensure that the property address and legal description are correct. An inaccurate description can lead to delays or even rejection of the deed.

Another frequent mistake is not including all necessary parties in the document. If there are co-owners or other interested parties, their signatures are often required. Omitting a necessary signature can invalidate the deed and prolong the foreclosure process.

Many individuals also overlook the importance of ensuring that the deed is notarized. A notary public must witness the signing of the document to make it legally binding. Without this step, the deed may not be recognized by the lender or the court.

In addition, people often fail to understand the implications of the deed. They may not realize that signing a deed in lieu of foreclosure can affect their credit score and future borrowing capabilities. It is crucial to fully comprehend the consequences before proceeding.

Another common mistake is neglecting to communicate with the lender throughout the process. Keeping the lender informed can help facilitate a smoother transaction. A lack of communication may result in misunderstandings or complications that could have been avoided.

Some individuals also forget to review their mortgage documents thoroughly. Understanding the terms of the mortgage can reveal whether a deed in lieu of foreclosure is a viable option. Ignoring this step can lead to unexpected challenges.

Additionally, people may not seek legal advice before completing the form. Consulting with a legal professional can provide valuable insights and help avoid pitfalls. Many individuals underestimate the benefits of having expert guidance during this process.

Another mistake is not considering tax implications. A deed in lieu of foreclosure can have tax consequences, and individuals should be aware of potential liabilities. Failing to account for these can lead to financial surprises later on.

Lastly, individuals often rush through the process, leading to careless errors. Taking the time to carefully fill out the form and double-check all information is vital. A thoughtful approach can prevent unnecessary complications and ensure a smoother transition.

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal document where a borrower voluntarily transfers property ownership to the lender to avoid foreclosure. |

| Governing Law | The process is governed by California Civil Code Sections 1475-1490. |

| Eligibility | Typically, borrowers facing financial hardship and unable to keep up with mortgage payments may consider this option. |

| Benefits | It can help borrowers avoid the lengthy foreclosure process and may have less negative impact on their credit score. |

| Risks | Borrowers may still be liable for any deficiency balance if the property sells for less than the mortgage amount. |

| Process | The borrower must submit a request to the lender, who will evaluate the situation before accepting the deed. |

| Documentation | Typically, the borrower must provide financial statements, hardship letters, and other relevant documentation. |

| Impact on Future Financing | While less damaging than foreclosure, a deed in lieu can still affect a borrower’s ability to secure future loans. |

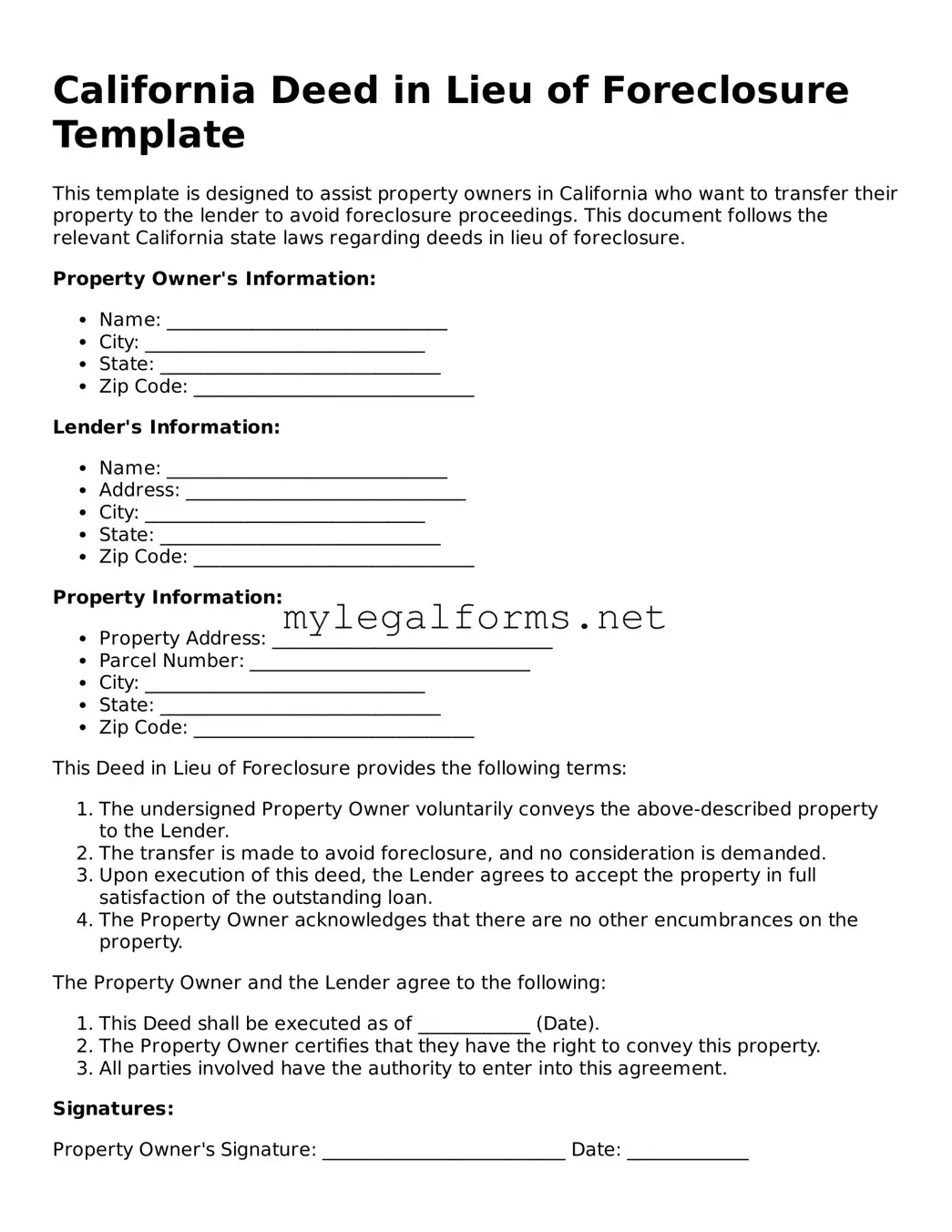

California Deed in Lieu of Foreclosure Template

This template is designed to assist property owners in California who want to transfer their property to the lender to avoid foreclosure proceedings. This document follows the relevant California state laws regarding deeds in lieu of foreclosure.

Property Owner's Information:

Lender's Information:

Property Information:

This Deed in Lieu of Foreclosure provides the following terms:

The Property Owner and the Lender agree to the following:

Signatures:

Property Owner's Signature: __________________________ Date: _____________

Lender's Signature: __________________________ Date: _____________

This document must be recorded with the county recorder’s office to be legally binding. It is recommended to seek legal advice before finalizing any agreements.