Promissory Note Document for California State

Promissory Note Document for California State

The California Promissory Note is a crucial financial document used to outline the terms of a loan between a borrower and a lender. This form serves as a written promise from the borrower to repay a specified amount of money, including any interest, within a predetermined timeframe. It includes essential details such as the loan amount, interest rate, repayment schedule, and any applicable late fees. Additionally, it addresses the rights and responsibilities of both parties, ensuring clarity and mutual understanding. This legally binding agreement can be tailored to suit various lending situations, whether it involves personal loans, business financing, or real estate transactions. By utilizing this form, both lenders and borrowers can protect their interests and establish a clear framework for repayment, fostering trust and accountability in their financial dealings.

When filling out and using the California Promissory Note form, it is important to understand the following key points:

By paying attention to these points, you can navigate the process of creating and using a promissory note with greater confidence.

Texas Promissory Note Template - In business, promissory notes can also aid in cash flow management.

Promissory Note Template Florida Pdf - Using a promissory note can help build trust and transparency in private lending situations.

The California Power of Attorney form is a legal document that allows an individual to designate another person to make decisions on their behalf. This form can cover a wide range of financial and healthcare matters, providing essential authority to the appointed agent. To further understand the importance and application of this document, you can visit https://californiadocsonline.com/power-of-attorney-form, which offers valuable insights for anyone considering this important legal tool.

Promissory Note for Personal Loan - Promissory notes can be secured or unsecured, depending on whether collateral is involved.

Simple Promissory Note - Can be revised if terms change, as long as both agree.

When dealing with a California Promissory Note, several other documents may be necessary to ensure a complete and legally sound transaction. Each of these documents serves a specific purpose and helps clarify the terms of the agreement between the parties involved. Below is a list of common forms and documents often used alongside a Promissory Note.

Understanding these documents can help you navigate the complexities of lending and borrowing in California. Each one plays a crucial role in protecting the interests of both parties and ensuring a clear understanding of the terms of the agreement. Always consider seeking legal advice to ensure compliance with state laws and regulations.

When filling out the California Promissory Note form, it is important to follow specific guidelines to ensure accuracy and compliance. Below are some key actions to take and avoid:

Filling out the California Promissory Note form can seem straightforward, but many individuals make critical mistakes that could lead to complications. One common error is failing to include the correct names of the borrower and lender. It’s essential that both parties are accurately identified to avoid disputes later.

Another frequent mistake is neglecting to specify the loan amount clearly. This figure should be stated in both numerical and written form. Omitting or misrepresenting this amount can create confusion and potential legal issues down the line.

Many people also overlook the importance of detailing the interest rate. If the interest rate is not clearly defined, it could lead to misunderstandings regarding repayment obligations. In California, the maximum allowable interest rate should be adhered to, so it’s crucial to double-check this information.

Inadequate descriptions of the repayment terms are another pitfall. It’s vital to outline when payments are due, how they should be made, and any grace periods. Vague language can lead to disagreements and complicate the enforcement of the note.

Some individuals fail to include a late payment penalty. This omission can be detrimental, as it may not provide sufficient motivation for timely payments. Clearly stating the consequences of late payments can help protect the lender’s interests.

Additionally, people often neglect to sign the document. A promissory note without signatures is not legally binding. Both the borrower and lender must sign to validate the agreement.

Another mistake is not having the document witnessed or notarized. While not always required, having a witness or notary can add an extra layer of protection and legitimacy to the agreement.

Some individuals also forget to include a default clause. This clause is essential as it outlines what happens if the borrower fails to make payments. Without this provision, the lender may find it challenging to enforce their rights in case of default.

Moreover, failing to keep copies of the signed document is a common oversight. Both parties should retain a copy for their records. This ensures that everyone has access to the same information and can refer back to the original terms if necessary.

Finally, many individuals rush through the process without reading the entire document carefully. Taking the time to review the entire promissory note can help catch errors and ensure that all terms are understood. A thorough review can prevent costly misunderstandings in the future.

| Fact Name | Details |

|---|---|

| Definition | A California promissory note is a written promise to pay a specific amount of money at a defined time. |

| Governing Law | California Civil Code Sections 3300-3400 govern promissory notes in California. |

| Parties Involved | The document involves two main parties: the borrower (maker) and the lender (payee). |

| Interest Rate | Interest rates can be fixed or variable and must comply with California usury laws. |

| Payment Terms | The note should clearly outline the payment schedule, including due dates and amounts. |

| Default Clause | Many promissory notes include a default clause, specifying the consequences if the borrower fails to make payments. |

| Secured vs. Unsecured | Promissory notes can be secured by collateral or unsecured, impacting the lender's rights in case of default. |

| Signatures Required | The note must be signed by the borrower to be legally binding, and it’s advisable for the lender to sign as well. |

| State-Specific Requirements | California requires certain disclosures in the note, particularly when it involves consumer loans. |

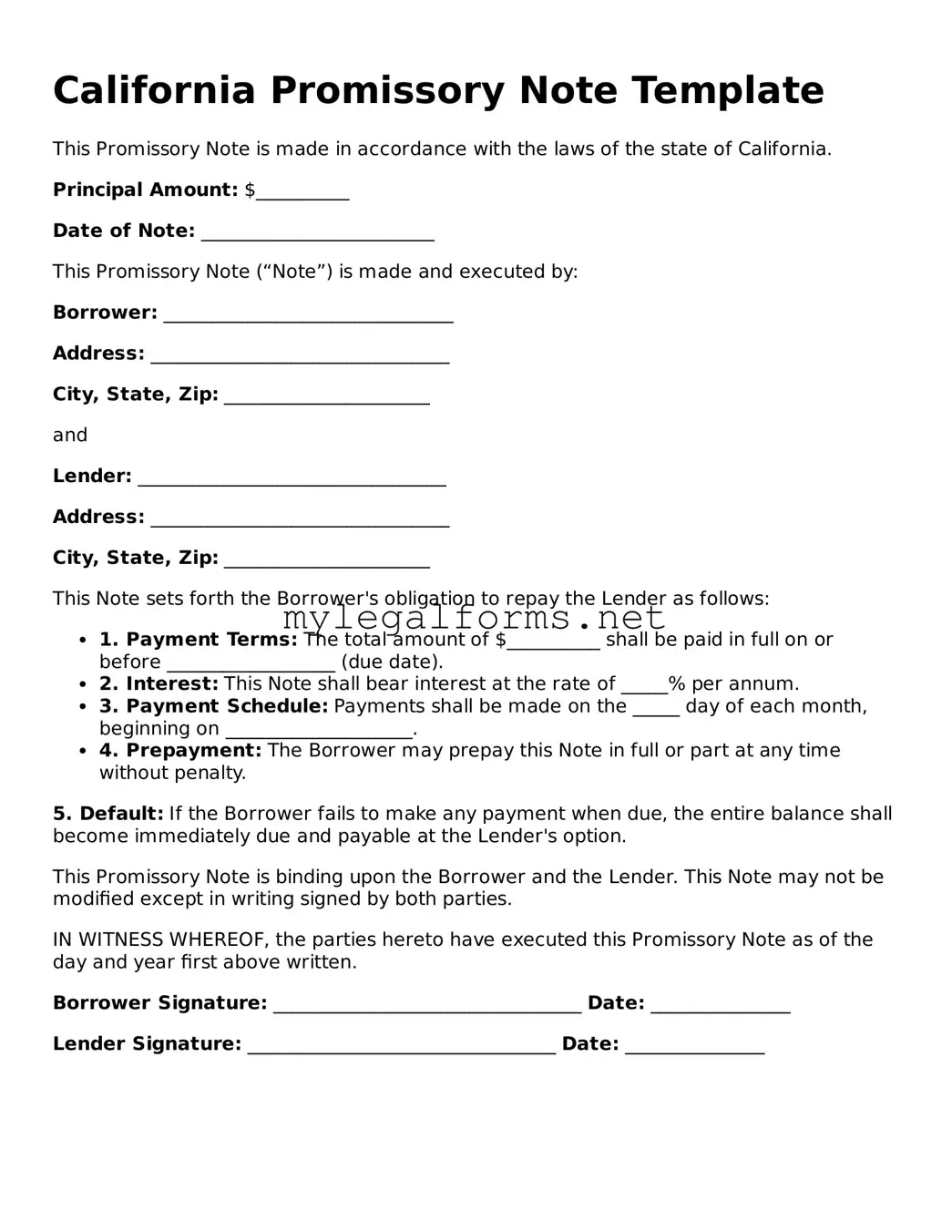

California Promissory Note Template

This Promissory Note is made in accordance with the laws of the state of California.

Principal Amount: $__________

Date of Note: _________________________

This Promissory Note (“Note”) is made and executed by:

Borrower: _______________________________

Address: ________________________________

City, State, Zip: ______________________

and

Lender: _________________________________

Address: ________________________________

City, State, Zip: ______________________

This Note sets forth the Borrower's obligation to repay the Lender as follows:

5. Default: If the Borrower fails to make any payment when due, the entire balance shall become immediately due and payable at the Lender's option.

This Promissory Note is binding upon the Borrower and the Lender. This Note may not be modified except in writing signed by both parties.

IN WITNESS WHEREOF, the parties hereto have executed this Promissory Note as of the day and year first above written.

Borrower Signature: _________________________________ Date: _______________

Lender Signature: _________________________________ Date: _______________