Attorney-Approved Employee Loan Agreement Form

Attorney-Approved Employee Loan Agreement Form

The Employee Loan Agreement form serves as a crucial document in the relationship between employers and employees, particularly when financial assistance is extended to staff members. This form outlines the terms and conditions under which a loan is provided, ensuring both parties have a clear understanding of their obligations. Key aspects typically included in this agreement are the loan amount, interest rate, repayment schedule, and any applicable fees. Additionally, the form may specify the consequences of defaulting on the loan, such as deductions from future paychecks or other actions that may be taken to recover the funds. By clearly defining these elements, the Employee Loan Agreement helps to protect the interests of both the employer and the employee, fostering transparency and trust in the lending process. Furthermore, it is important for employees to carefully review the terms before signing, as this agreement can have significant financial implications for their future. Overall, a well-structured Employee Loan Agreement is essential for facilitating responsible lending practices within the workplace.

When filling out and using the Employee Loan Agreement form, keep these key takeaways in mind:

When managing employee loans, several forms and documents are typically used alongside the Employee Loan Agreement. Each of these documents serves a specific purpose, ensuring that both the employer and employee understand their rights and responsibilities. Here’s a brief overview of some commonly used forms:

Using these documents in conjunction with the Employee Loan Agreement can create a clear framework for managing loans within the workplace. Each form plays a crucial role in protecting both the employee and the employer, fostering transparency and accountability in financial transactions.

When filling out the Employee Loan Agreement form, it’s important to approach the task with care. Here are some key do's and don'ts to keep in mind:

When completing the Employee Loan Agreement form, individuals often overlook key details that can lead to complications. One common mistake is failing to provide accurate personal information. This includes not using the correct legal name, which can cause issues in the future. Ensure that all names and contact details are up-to-date and correctly spelled.

Another frequent error is neglecting to specify the loan amount. It is crucial to clearly state how much money is being borrowed. Without this information, the agreement may be deemed incomplete or invalid. Double-check the figures to avoid misunderstandings later on.

People sometimes forget to outline the repayment terms. This includes the schedule for payments and the interest rate, if applicable. Clearly defining these terms helps prevent disputes and ensures that both parties understand their obligations. Missing this information can lead to confusion and potential financial strain.

Additionally, some individuals do not sign the form. A signature is essential for the agreement to be legally binding. Without it, the document holds no value. Always remember to sign and date the form before submission.

Another mistake is not keeping a copy of the signed agreement. After filling out the form, it is important to retain a copy for personal records. This can serve as proof of the agreement and provide clarity if questions arise in the future.

Lastly, people may overlook the need for a witness or notary, depending on company policy. Some agreements require a third party to verify the signatures. Failing to have this step completed can render the agreement unenforceable. Be sure to check the requirements before finalizing the document.

| Fact Name | Description |

|---|---|

| Definition | An Employee Loan Agreement is a contract between an employer and an employee regarding the terms of a loan provided by the employer. |

| Purpose | This agreement outlines the loan amount, repayment terms, interest rates, and any other conditions that apply. |

| Legal Binding | Once signed, the agreement is legally binding, meaning both parties must adhere to the terms outlined. |

| State-Specific Forms | Some states may have specific requirements or forms for employee loan agreements. Check local laws for compliance. |

| Governing Law | The agreement is typically governed by the laws of the state in which the employee works, such as California or New York. |

| Repayment Terms | Repayment terms should clearly state the schedule, including start date and frequency of payments. |

| Interest Rates | The agreement may specify whether the loan will accrue interest and at what rate, if applicable. |

| Default Conditions | It is important to outline what constitutes a default on the loan and the consequences thereof. |

| Confidentiality | Confidentiality clauses may be included to protect the privacy of both parties regarding the loan terms. |

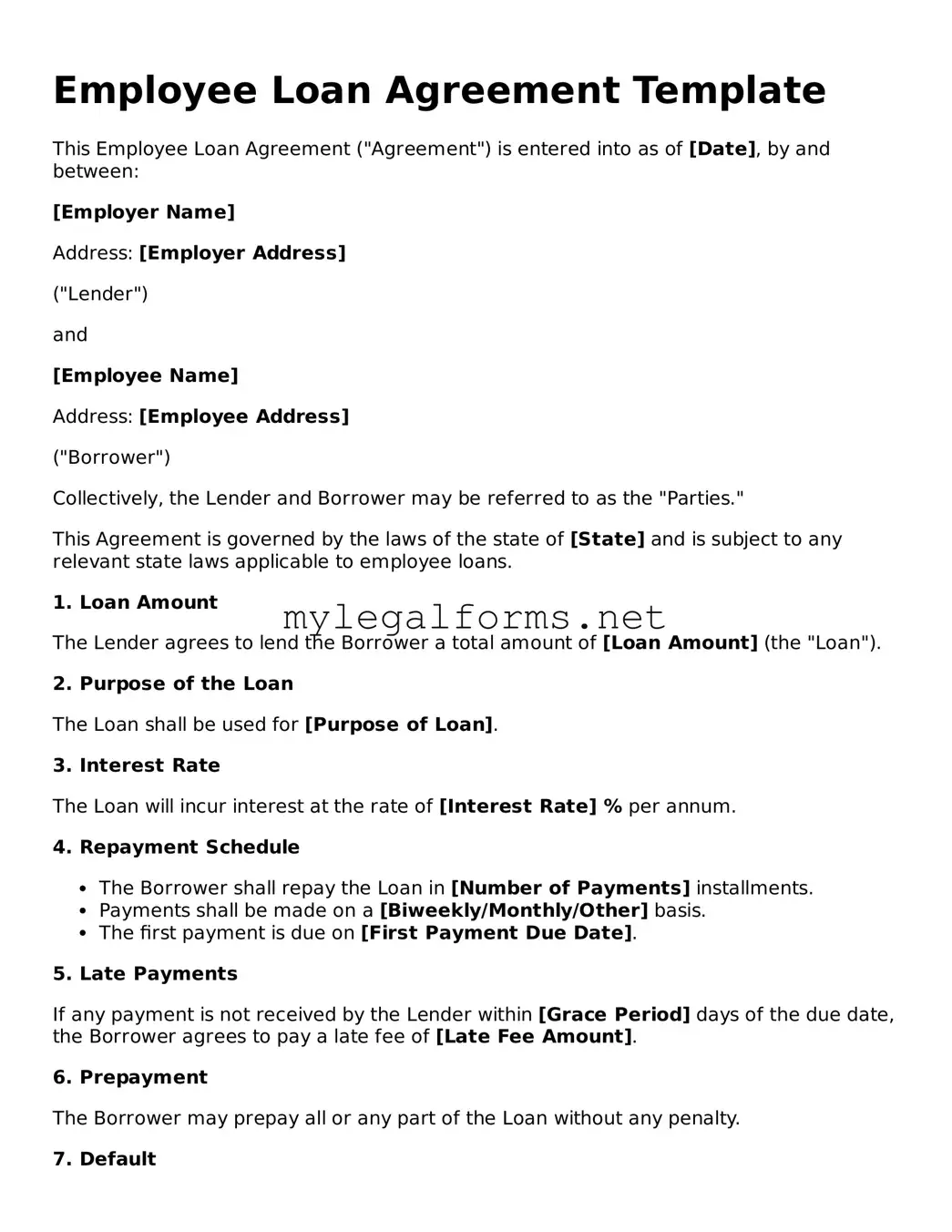

Employee Loan Agreement Template

This Employee Loan Agreement ("Agreement") is entered into as of [Date], by and between:

[Employer Name]

Address: [Employer Address]

("Lender")

and

[Employee Name]

Address: [Employee Address]

("Borrower")

Collectively, the Lender and Borrower may be referred to as the "Parties."

This Agreement is governed by the laws of the state of [State] and is subject to any relevant state laws applicable to employee loans.

1. Loan Amount

The Lender agrees to lend the Borrower a total amount of [Loan Amount] (the "Loan").

2. Purpose of the Loan

The Loan shall be used for [Purpose of Loan].

3. Interest Rate

The Loan will incur interest at the rate of [Interest Rate] % per annum.

4. Repayment Schedule

5. Late Payments

If any payment is not received by the Lender within [Grace Period] days of the due date, the Borrower agrees to pay a late fee of [Late Fee Amount].

6. Prepayment

The Borrower may prepay all or any part of the Loan without any penalty.

7. Default

If the Borrower fails to make any payment when due, the Lender may declare the entire Loan amount due and payable.

8. Governing Law

This Agreement shall be governed by the laws of the state of [State], without regard to its conflict of laws principles.

9. Amendments

This Agreement may only be amended in writing, signed by both Parties.

IN WITNESS WHEREOF, the Parties have executed this Employee Loan Agreement as of the date first above written.

Employer:

__________________________

Signature

__________________________

Name

__________________________

Title

Employee:

__________________________

Signature

__________________________

Name

This document is provided as a template and may not cover all circumstances. It is advisable for Parties to seek legal counsel before entering into any agreement.