Fl Dr 312 Template

Fl Dr 312 Template

The Florida Form DR-312, known as the Affidavit of No Florida Estate Tax Due, plays a crucial role in the estate administration process for individuals who have recently lost a loved one. This form serves as a declaration by the personal representative of the estate, confirming that no Florida estate tax is owed and that a federal estate tax return is not required. It is essential for personal representatives to accurately complete this affidavit, as it provides legal proof of nonliability for estate tax, effectively removing any lien the Florida Department of Revenue may have on the estate. The form requires specific details, including the decedent's name, date of death, and their domicile at the time of passing. Additionally, the personal representative must acknowledge their responsibility for the distribution of estate property. Proper filing of Form DR-312 with the appropriate clerk of the circuit court is imperative, as it ensures that the estate is free from tax obligations and that the decedent's property can be distributed without delay. Understanding the significance and requirements of this form is vital for anyone navigating the complexities of estate management in Florida.

The DR-312 form is used to declare that no Florida estate tax is due for a decedent's estate.

It must be filed with the clerk of the circuit court in the county where the decedent owned property.

Do not send the form to the Florida Department of Revenue.

The form is applicable when a federal estate tax return (Form 706 or 706-NA) is not required.

Personal representatives, as defined by Florida law, must complete the form.

The affidavit serves as evidence of nonliability for Florida estate tax and can remove the estate tax lien.

It is crucial to ensure that the case style of the estate probate proceeding is included in the designated space on the form.

The form cannot be used for estates that are required to file a federal Form 706 or 706-NA.

For assistance or questions, contact Taxpayer Services at 850-488-6800.

Free Lease Agreement Florida Template - Common areas of the property are also defined, granting tenants the right to use them during the lease term.

For those in need of assistance with the Sample Tax Return Transcript form, it is helpful to refer to resources like Formaid Org, which offer guidance on how to navigate and utilize this important document effectively. Understanding this form can greatly aid in confirming the accuracy of one's tax filings and understanding any adjustments that may have been made by the IRS.

Irs 433-f Allowable Expenses - Completing the form may require gathering various financial documents.

The Fl Dr 312 form, known as the Affidavit of No Florida Estate Tax Due, is an important document in the estate administration process in Florida. It serves to confirm that an estate is not liable for Florida estate tax and that no federal estate tax return is required. Along with this form, several other documents may be necessary to facilitate the probate process. Below is a list of additional forms and documents that are often used in conjunction with the Fl Dr 312 form.

Understanding these forms and documents is crucial for anyone navigating the probate process in Florida. Each plays a specific role in ensuring that the estate is settled in accordance with the law, and that all obligations are met. Proper completion and filing of these documents can help streamline the administration of the estate and avoid potential legal complications.

When completing the Florida Form DR-312, it is essential to follow specific guidelines to ensure the process goes smoothly. Here are six things you should and shouldn't do:

Filling out the Florida DR-312 form, also known as the Affidavit of No Florida Estate Tax Due, can be straightforward, but many people make common mistakes that can complicate the process. One significant error occurs when individuals fail to accurately identify themselves as the personal representative of the estate. This section requires the printed name of the personal representative, and omitting or misspelling this information can lead to delays or rejections.

Another frequent mistake involves the date of death. The form requires a specific format for entering this date. If individuals do not follow the format (month/day/year), it can create confusion and may result in the form being returned. Ensuring that the date is clear and correctly formatted is crucial for the validity of the affidavit.

People often overlook the requirement to indicate the decedent's citizenship status. This section must be checked accurately, either as a U.S. citizen or not. Failing to check one of the boxes can lead to questions about the estate's tax obligations, potentially complicating the filing process.

Additionally, some individuals misunderstand the implications of the federal estate tax return requirement. The form clearly states that a federal estate tax return is not required for the estate. However, if individuals mistakenly believe they need to file one, they may hesitate to submit the DR-312, delaying the process unnecessarily.

Another common error is the lack of a signature or failure to provide the correct printed name and contact information. The form must be signed by the personal representative, and any missing or incorrect information can cause issues. It is essential to double-check that all signatures are present and that the printed name matches the signature.

Finally, many people neglect to file the form with the appropriate clerk of the court. Instead, they might mistakenly mail it to the Florida Department of Revenue. This error can lead to significant delays in processing the affidavit and may result in additional complications regarding the estate's tax status.

| Fact Name | Details |

|---|---|

| Form Title | Affidavit of No Florida Estate Tax Due DR-312 |

| Governing Law | Chapter 198, Florida Statutes and Rule 12C-3.008, Florida Administrative Code |

| Effective Date | Effective as of January 2021 |

| Purpose | This form is used to declare that no Florida estate tax is due for the estate of the decedent. |

| Eligibility | Applicable when no federal estate tax return (Form 706 or 706-NA) is required to be filed. |

| Filing Location | The form must be filed with the clerk of the circuit court in the county where the decedent owned property. |

| Liability Acknowledgment | The personal representative acknowledges liability for any distributions made from the estate. |

| Nonliability Evidence | Filing this form serves as evidence of nonliability for Florida estate tax and removes any estate tax lien. |

| Restrictions | This form cannot be used for estates that are required to file federal Form 706 or 706-NA. |

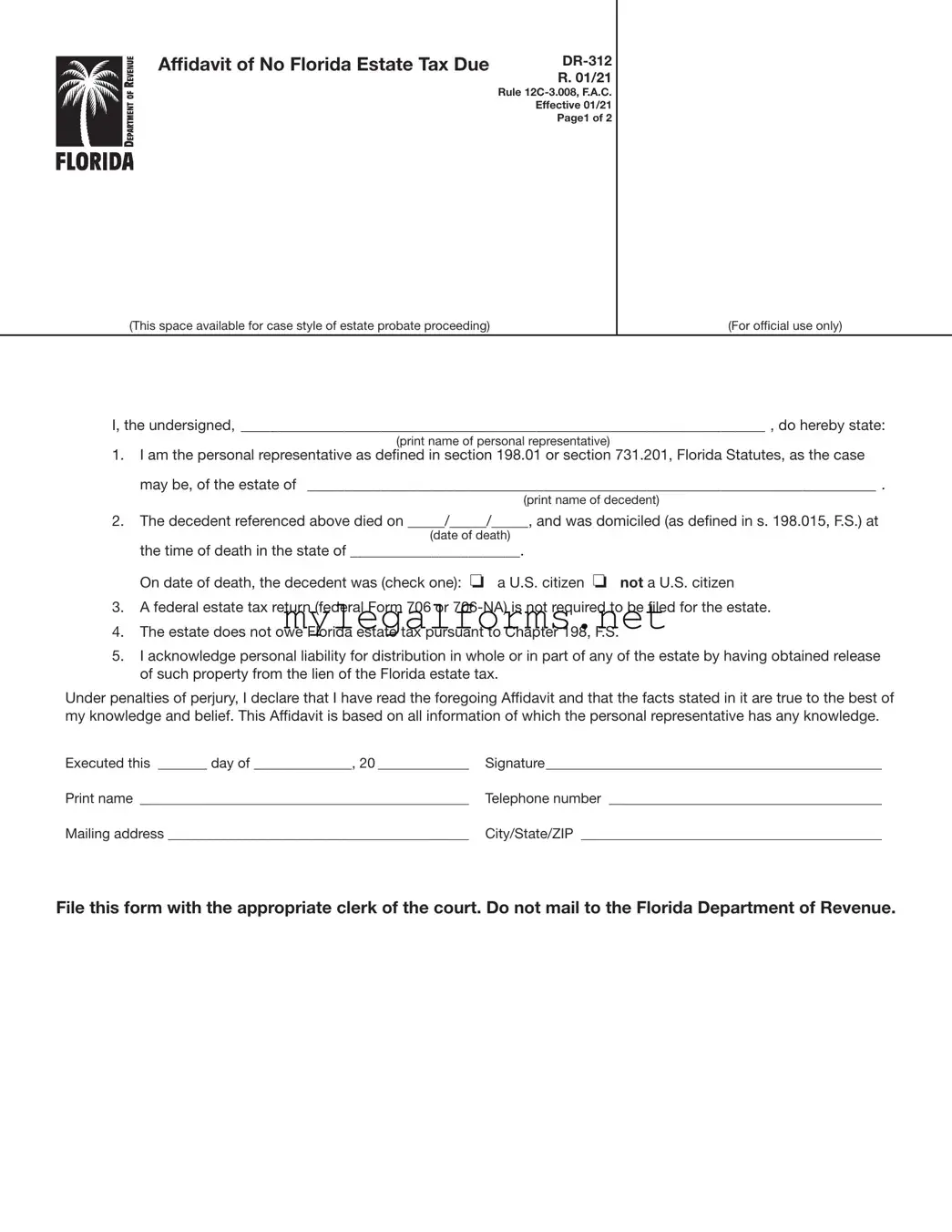

Affidavit of No Florida Estate Tax Due

Rule

Effective 01/21

Page1 of 2

(This space available for case style of estate probate proceeding) |

(For official use only) |

I, the undersigned, _______________________________________________________________________ , do hereby state:

(print name of personal representative)

1.I am the personal representative as defined in section 198.01 or section 731.201, Florida Statutes, as the case may be, of the estate of _____________________________________________________________________________ .

(print name of decedent)

2.The decedent referenced above died on _____/_____/_____, and was domiciled (as defined in s. 198.015, F.S.) at

(date of death)

the time of death in the state of _______________________.

On date of death, the decedent was (check one): o a U.S. citizen o not a U.S. citizen

3.A federal estate tax return (federal Form 706 or

4.The estate does not owe Florida estate tax pursuant to Chapter 198, F.S.

5.I acknowledge personal liability for distribution in whole or in part of any of the estate by having obtained release of such property from the lien of the Florida estate tax.

Under penalties of perjury, I declare that I have read the foregoing Affidavit and that the facts stated in it are true to the best of my knowledge and belief. This Affidavit is based on all information of which the personal representative has any knowledge.

Executed this _______ day of ______________, 20 _____________ |

Signature________________________________________________ |

Print name _______________________________________________ |

Telephone number _______________________________________ |

Mailing address ___________________________________________ |

City/State/ZIP ___________________________________________ |

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

R. 01/21

Page 2 of 2

Instructions for Completing Form

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

General Information

If Florida estate tax is not due and a federal estate tax return (federal Form 706 or

Form

The

Where to File Form

Form

When to Use Form

Form

and a federal estate tax return (federal Form 706 or

Federal thresholds for filing federal Form 706 only: (For informational purposes only. Please confirm with Form 706 instructions.)

Date of Death |

Dollar Threshold |

(year) |

for Filing Form 706 |

|

(value of gross estate) |

|

|

2000 and 2001 |

$675,000 |

|

|

2002 and 2003 |

$1,000,000 |

|

|

2004 and 2005 |

$1,500,000 |

|

|

For 2006 and forward |

|

go to the IRS website at |

|

www.irs.gov to obtain |

|

thresholds. |

|

|

|

For thresholds for filing federal Form

If an administration proceeding is pending for an estate, Form

To Contact Us

Information, forms, and tutorials are available on the Department’s website floridarevenue.com

If you have any questions, or need assistance, call Taxpayer Services at

To find a taxpayer service center near you, go to: floridarevenue.com/taxes/servicecenters

For written replies to tax questions, write to: Taxpayer Services - Mail Stop

5050 W Tennessee St Tallahassee FL

Subscribe to Receive Email Alerts from the Department.

Subscribe to receive an email when Tax Information Publications and proposed rules are posted to the Department’s website. Subscribe today at floridarevenue.com/dor/subscribe.

Reference Material

Rule Chapter