Attorney-Approved Loan Agreement Form

Attorney-Approved Loan Agreement Form

A Loan Agreement form serves as a critical document in the lending process, establishing the terms and conditions under which a borrower receives funds from a lender. It outlines essential details such as the loan amount, interest rate, repayment schedule, and any collateral required. By clearly defining the rights and responsibilities of both parties, the form helps prevent misunderstandings and disputes. Additionally, it may include clauses related to late fees, default conditions, and prepayment options, ensuring that both the lender and borrower are fully aware of their obligations. This comprehensive approach not only protects the interests of the lender but also provides the borrower with a clear roadmap for repayment. Understanding the components of a Loan Agreement form is vital for anyone involved in a lending transaction, as it lays the groundwork for a successful financial relationship.

When filling out and using a Loan Agreement form, it is essential to understand the key components to ensure clarity and enforceability. Here are seven important takeaways:

Florida Power Attorney - Authorizes another person to manage your vehicle's registration expiration.

Adoption Recommendation Letter - Shares the applicant's vision for the future they wish to provide a child.

When entering into a loan agreement, various forms and documents may accompany it to ensure clarity and protection for all parties involved. Each of these documents serves a specific purpose and contributes to the overall understanding of the loan terms and conditions.

Understanding these documents can help borrowers and lenders navigate the complexities of a loan agreement. Each plays a crucial role in establishing the terms and protecting the interests of both parties throughout the lending process.

When filling out a Loan Agreement form, attention to detail is crucial. Here are some important dos and don’ts to keep in mind:

Filling out a Loan Agreement form can be a straightforward process, but many individuals make common mistakes that can lead to complications later on. One frequent error is failing to provide accurate personal information. Borrowers should ensure that their names, addresses, and contact details are correct. Inaccuracies can delay processing and create confusion during communication.

Another mistake involves overlooking the loan amount. Borrowers may either request too much or too little. It's essential to carefully calculate the needed funds and ensure that the requested amount aligns with the purpose of the loan. Misjudging this figure can lead to financial strain or missed opportunities.

Many people neglect to read the terms and conditions thoroughly. Each loan agreement contains specific clauses that outline repayment schedules, interest rates, and penalties for late payments. Ignoring these details can result in unexpected costs or unfavorable terms. It’s advisable to understand what one is agreeing to before signing.

In addition, some borrowers fail to consider their repayment capacity. Individuals should evaluate their financial situation realistically. Taking on a loan without a clear repayment plan can lead to default and damage credit scores. A budget review can help in determining what is manageable.

Another common oversight is not providing the required documentation. Lenders often request proof of income, identification, and other financial records. Failing to submit these documents can delay the approval process or lead to outright denial of the loan.

Additionally, some borrowers skip the comparison of loan offers. Each lender may provide different terms and rates. By not shopping around, individuals might miss out on better deals that could save them money in the long run.

People often forget to ask questions. If any part of the loan agreement is unclear, borrowers should seek clarification. Misunderstandings can lead to costly mistakes or unmet expectations.

Furthermore, some individuals do not consider the impact of their credit score. A low credit score can result in higher interest rates or loan denial. It’s wise to check credit reports and address any issues before applying for a loan.

Lastly, rushing through the process can lead to errors. Taking the time to review the form carefully can prevent mistakes. A thorough check can ensure that all information is accurate and complete, ultimately making the loan process smoother.

| Fact Name | Description |

|---|---|

| Purpose | A Loan Agreement form outlines the terms and conditions under which a borrower receives funds from a lender. |

| Parties Involved | The form typically includes details about the borrower and the lender, including their names and contact information. |

| Governing Law | The agreement is subject to the laws of the state in which it is executed, which can vary significantly. For example, in California, it follows California Civil Code Section 1916. |

| Key Terms | Important terms such as the loan amount, interest rate, repayment schedule, and any collateral should be clearly defined. |

| Signatures | The agreement must be signed by both parties to be legally binding, indicating their acceptance of the terms. |

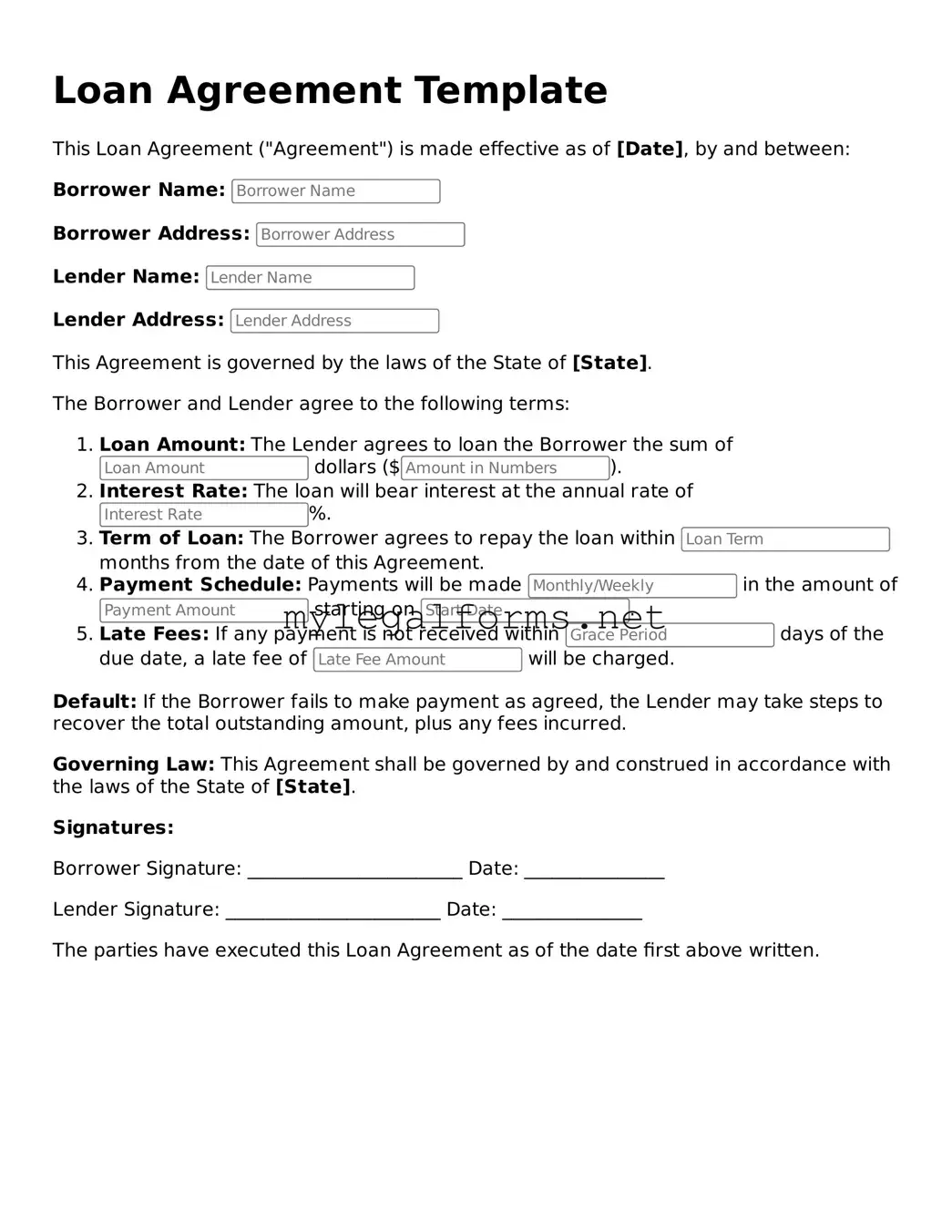

Loan Agreement Template

This Loan Agreement ("Agreement") is made effective as of [Date], by and between:

Borrower Name:

Borrower Address:

Lender Name:

Lender Address:

This Agreement is governed by the laws of the State of [State].

The Borrower and Lender agree to the following terms:

Default: If the Borrower fails to make payment as agreed, the Lender may take steps to recover the total outstanding amount, plus any fees incurred.

Governing Law: This Agreement shall be governed by and construed in accordance with the laws of the State of [State].

Signatures:

Borrower Signature: _______________________ Date: _______________

Lender Signature: _______________________ Date: _______________

The parties have executed this Loan Agreement as of the date first above written.