Attorney-Approved Promissory Note for a Car Form

Attorney-Approved Promissory Note for a Car Form

When purchasing a vehicle, a Promissory Note for a Car serves as a crucial financial document that outlines the agreement between the buyer and the lender. This form typically includes essential details such as the total loan amount, interest rate, repayment schedule, and consequences for late payments or default. It not only solidifies the buyer's commitment to repay the borrowed funds but also protects the lender's interests. Key components of the note often encompass the names and addresses of both parties, a clear description of the vehicle being financed, and the specific terms under which the loan will be repaid. By signing this document, the buyer acknowledges their obligation to fulfill the payment terms, while the lender retains the right to reclaim the vehicle if the buyer fails to comply. Understanding the intricacies of this form is vital for both parties, as it lays the groundwork for a transparent and legally binding financial transaction.

When filling out and using the Promissory Note for a Car form, it's important to keep several key points in mind to ensure clarity and legal validity.

By following these guidelines, both parties can feel more secure in their agreement and maintain a clear understanding of their obligations.

Release of Promissory Note Template - A legal release that eliminates further claims related to a loan.

In order to create a comprehensive understanding of loan agreements in New York, individuals often seek resources that offer templates for essential documents. For those interested in structuring their repayment terms accurately, utilizing a New York Promissory Note is highly beneficial. This formal document not only details the amount to be repaid but also clarifies the responsibilities of both parties involved in the transaction. For further assistance, you can find helpful resources through All New York Forms, ensuring that you have the right tools to protect your financial interests.

A Promissory Note for a Car is often part of a larger set of documents required during a vehicle purchase or financing process. Below is a list of other forms and documents that may accompany a Promissory Note, each serving a specific purpose in the transaction.

These documents collectively facilitate the legal transfer of ownership and ensure that all parties understand their rights and responsibilities in the transaction. Properly managing these forms can help avoid potential disputes and ensure a smooth vehicle purchase process.

When filling out the Promissory Note for a Car form, it is essential to be careful and thorough. Here are ten important tips to consider:

Filling out a Promissory Note for a Car can be a straightforward process, but many people make common mistakes that can lead to complications down the line. One frequent error is not including the correct names of the parties involved. It’s essential to clearly state the names of both the borrower and the lender. Misspellings or incorrect names can create confusion and potentially invalidate the agreement.

Another mistake often seen is failing to specify the loan amount. This figure should be clearly stated in both numerical and written form. Omitting this detail can lead to disputes about how much money is actually being borrowed, which can complicate repayment terms.

Many individuals neglect to include the interest rate in their Promissory Note. This rate should be clearly defined and agreed upon by both parties. Without this information, the lender may face difficulties in collecting the agreed-upon interest, and the borrower may be unsure of their total repayment obligation.

Some people overlook the importance of outlining the repayment schedule. It is crucial to specify when payments are due, how much each payment will be, and the total duration of the loan. A vague repayment schedule can lead to misunderstandings and missed payments.

Another common oversight is not including a clause for late payments. This clause can stipulate penalties or additional interest that may accrue if payments are not made on time. Without this provision, the lender may have limited recourse if the borrower fails to meet their obligations.

Additionally, individuals often forget to sign and date the document. A Promissory Note is not legally binding unless it is signed by both parties. Failing to do so can render the agreement unenforceable, leaving both parties unprotected.

Some borrowers may mistakenly think that a verbal agreement is sufficient. Relying solely on verbal promises can lead to misunderstandings. A written Promissory Note serves as a clear record of the terms agreed upon, providing security for both parties.

People also frequently neglect to include a section for witnesses or notarization. Depending on state laws, having a witness or a notary public can add an extra layer of legitimacy to the document, making it harder for either party to dispute the agreement later on.

Another common error is not reviewing the document thoroughly before signing. Skimming through the terms can lead to overlooking important details. Taking the time to read the entire Promissory Note ensures that both parties understand their rights and obligations.

Lastly, some individuals fail to keep copies of the signed Promissory Note. It’s vital for both the lender and the borrower to retain a copy of the agreement for their records. This documentation can be crucial in case of future disputes or misunderstandings.

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a written promise to pay a specified amount of money to a lender for the purchase of a vehicle. |

| Parties Involved | The document involves two main parties: the borrower (buyer) and the lender (financial institution or individual). |

| Governing Law | The laws governing promissory notes vary by state. For instance, in California, the Uniform Commercial Code (UCC) applies. |

| Interest Rate | The note typically includes an interest rate, which can be fixed or variable, affecting the total repayment amount. |

| Payment Terms | Payment terms outline how often payments are made (monthly, bi-weekly) and the duration of the loan. |

| Default Consequences | If the borrower fails to make payments, the lender has the right to take legal action or repossess the vehicle. |

| Signatures Required | Both parties must sign the promissory note for it to be legally binding, indicating their agreement to the terms. |

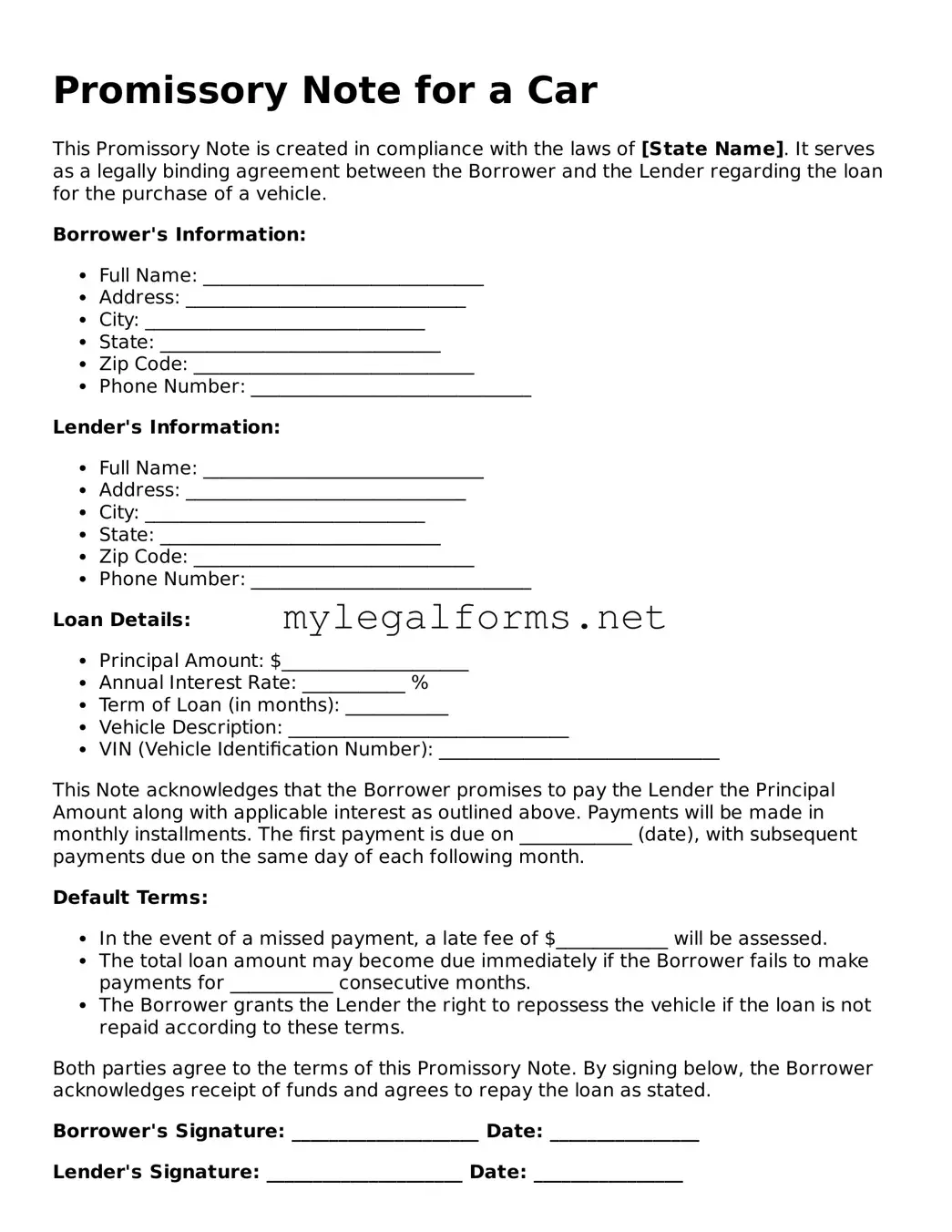

Promissory Note for a Car

This Promissory Note is created in compliance with the laws of [State Name]. It serves as a legally binding agreement between the Borrower and the Lender regarding the loan for the purchase of a vehicle.

Borrower's Information:

Lender's Information:

Loan Details:

This Note acknowledges that the Borrower promises to pay the Lender the Principal Amount along with applicable interest as outlined above. Payments will be made in monthly installments. The first payment is due on ____________ (date), with subsequent payments due on the same day of each following month.

Default Terms:

Both parties agree to the terms of this Promissory Note. By signing below, the Borrower acknowledges receipt of funds and agrees to repay the loan as stated.

Borrower's Signature: ____________________ Date: ________________

Lender's Signature: _____________________ Date: ________________

This document will serve as a record of the borrowing arrangement and the details surrounding the vehicle loan.